If you have been trying to figure out how to start investing, you have probably come across these two terms more times than you can count.

Mutual fund vs index fund. Which one should a beginner actually put their money into? And what is even the real difference between the two?

Here is the truth: most people overcomplicate this decision. Once you understand what each one actually does and how they work in the real world, the choice becomes a lot clearer.

This guide will walk you through everything you need to know, in plain English, so you can make a confident decision with your money.

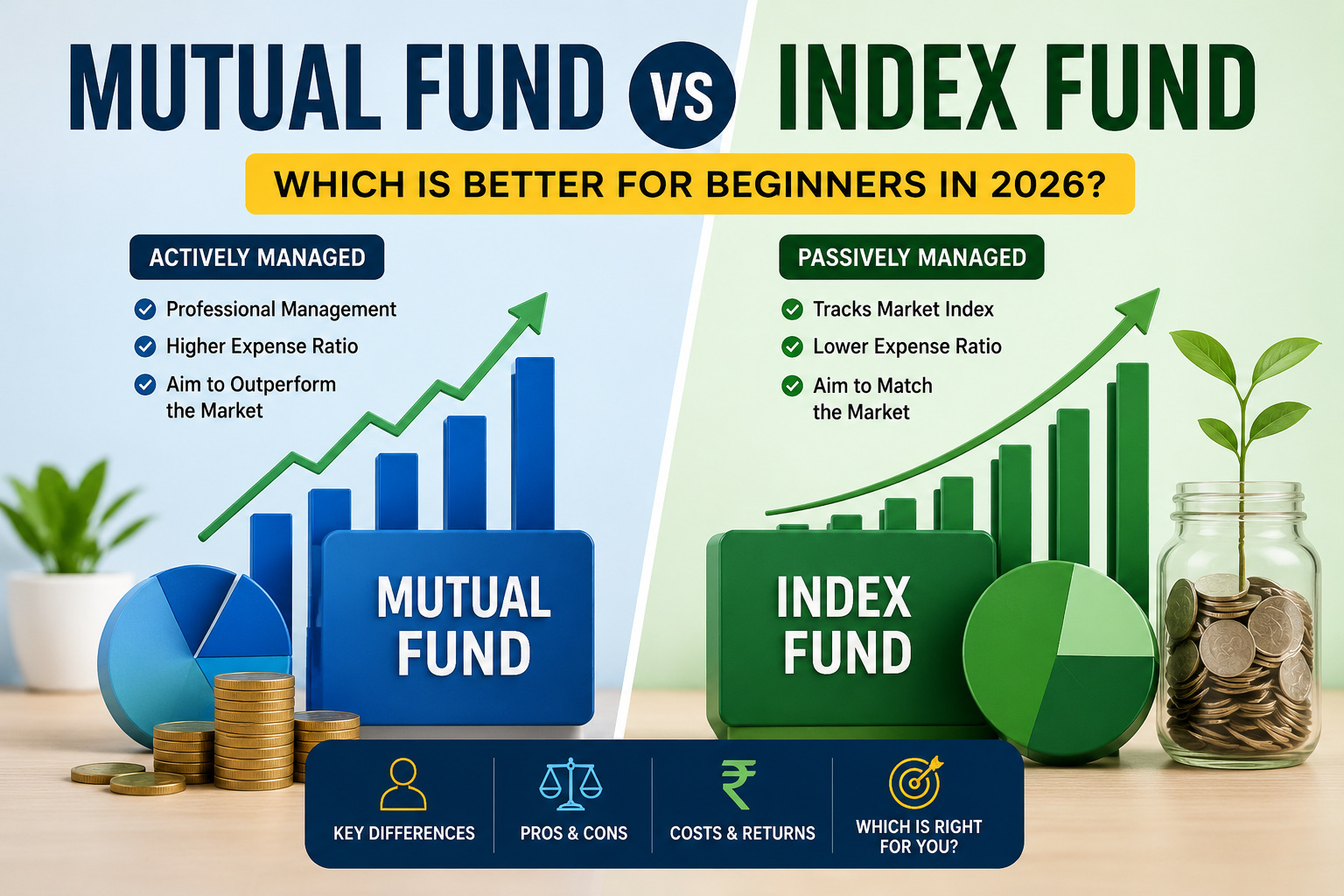

What Is a Mutual Fund?

A mutual fund is a pool of money collected from many investors that gets invested into a mix of stocks, bonds, or other assets. Think of it like a giant pot of money that a professional fund manager controls. That manager decides what to buy, when to sell, and how to build the overall portfolio.

The idea sounds great on paper. You hand over your money to someone with years of experience and they do all the heavy lifting for you. But there is a catch, which we will get to in a moment.

How Actively Managed Mutual Funds Work?

Most mutual funds are actively managed, meaning a team of analysts and portfolio managers are constantly researching companies, studying market trends, and making buy and sell decisions. Their goal is to beat the market and deliver better returns than average.

You pay for this expertise through something called an expense ratio, which is an annual fee that gets taken out of your investment returns. Expense ratios for actively managed mutual funds can range anywhere from 0.5% to upwards of 1.5% or more per year. That might not sound like a lot, but compounded over 20 or 30 years, it can eat into tens of thousands of dollars of your potential gains.

ALSO READ: GoMyFinance.com Saving Money: Guide to Finally Building Real Savings

What Is an Index Fund?

An index fund is a type of fund that simply tracks a market index, like the S&P 500 or the total stock market. Instead of having a manager pick and choose stocks, the fund automatically holds all or most of the stocks in that index in the same proportions.

There is no guesswork, no active decision making, and no expensive team of analysts behind the scenes. The fund just mirrors the index. If the S&P 500 goes up, your index fund goes up by roughly the same amount. If it drops, yours drops too.

Because index funds are passively managed, their fees are significantly lower. Many index funds charge expense ratios as low as 0.03% to 0.20% per year. That is a massive difference compared to actively managed mutual funds.

Are Index Funds and ETFs the Same Thing?

Not exactly, though they are closely related. An ETF (exchange-traded fund) is a type of index fund that trades on the stock market throughout the day like an individual stock. A traditional index fund is bought and sold at the end of the trading day at a set price. For most beginners, this difference is pretty minor, but it is worth knowing.

Mutual Fund vs Index Fund: The Key Differences That Actually Matter

Let us break down the most important differences so you can see exactly what you are comparing.

1. Cost: This Is Where Index Funds Win Easily

This is probably the single most important difference for beginners. Index funds are cheap to own. Actively managed mutual funds are expensive. Over a long investing timeline, fees matter more than almost any other single factor.

A 1% annual fee might feel small today, but on a $100,000 portfolio over 30 years, it could cost you well over $200,000 in lost growth compared to a low-fee index fund. That is real money that stays in your pocket when you go with the lower-cost option.

2. Performance: The Data Does Not Lie

Here is something that surprises a lot of new investors. Study after study has shown that the vast majority of actively managed mutual funds fail to beat the market over the long run. According to SPIVA research, roughly 80 to 90 percent of active fund managers underperform their benchmark index over a 15 to 20 year period.

Why? Because beating the market consistently is incredibly hard, even for professionals. After fees, taxes, and trading costs, most active funds end up lagging behind what a simple index fund would have returned. Index funds do not try to beat the market. They just keep up with it, and that turns out to be enough to outperform most active funds in the long run.

3. Simplicity: Index Funds Are Easier to Understand

When you invest in an S&P 500 index fund, you own a small piece of 500 of the largest American companies. Apple, Microsoft, Amazon, Google and hundreds more. That is instant diversification with a single purchase.

You do not need to analyze fund manager track records, study quarterly reports, or worry about strategy shifts. You set it, keep contributing, and let the market do its thing over time.

4. Tax Efficiency: Another Win for Index Funds

Actively managed mutual funds buy and sell stocks frequently, which triggers capital gains taxes inside the fund. Even if you did not sell your fund shares, you could still owe taxes at the end of the year just because of what the manager did inside the fund.

Index funds trade far less often, which means fewer taxable events and more of your money stays invested and growing.

When a Mutual Fund Might Actually Make Sense?

It would not be fair to say mutual funds are always a bad choice. There are some situations where they can still play a useful role.

i. Niche or specialty investing: Some actively managed funds focus on specific sectors, regions, or strategies that index funds do not cover well. If you want very targeted market exposure, an active fund might give you that.

ii. Bond and fixed income funds: Active management can sometimes add more value in the bond market compared to the stock market. Some financial advisors recommend active management specifically for the bond portion of a portfolio.

iii. Limited 401(k) options: Some employer retirement plans have limited investment choices and may not offer great index fund options. In that case, picking the lowest-cost mutual fund available is still a smart move.

Which Is Better for Beginners in 2026?

For most beginners starting their investing journey in 2026, index funds are the better starting point. The evidence points clearly in that direction, and here is why.

When you are just starting out, you do not have decades of market knowledge yet. You are still learning how the whole system works. The last thing you want is to be picking between dozens of actively managed funds, trying to figure out which manager has the best track record and whether their past performance will continue. That is stressful and, statistically speaking, a losing game.

Index funds take that decision almost entirely off the table. You pick one or two broad market index funds, keep contributing consistently, and do not overthink it. That simplicity is not just a convenience. It is actually an investing advantage, because it keeps you from making emotional decisions during market downturns.

A Few Index Funds Worth Looking Into for 2026

While this is not investment advice, these are some of the most widely used index funds among long-term investors.

1. Vanguard Total Stock Market Index Fund (VTSAX / VTI): Covers the entire U.S. stock market with very low fees. Great starting point for broad diversification.

2. Fidelity ZERO Total Market Index Fund (FZROX): Has a 0% expense ratio, making it one of the cheapest ways to invest in the market.

3. Schwab S&P 500 Index Fund (SWPPX): Tracks the S&P 500 with a rock-bottom expense ratio. Simple and effective for long-term investors.

How to Actually Get Started With Index Fund Investing?

Getting started is simpler than most people think. You do not need a financial advisor or a large lump sum to begin.

1. Open a brokerage account: Fidelity, Vanguard, and Charles Schwab are all excellent options with no account minimums for most index funds.

2. Start with tax-advantaged accounts first: If your employer offers a 401(k) with a match, grab that free money first. Then consider opening a Roth IRA for additional tax-free growth over time.

3. Pick one or two broad index funds: You do not need 10 different funds. A total market fund and an international index fund cover most of what the average beginner needs.

4. Set up automatic contributions: Automate a set amount each month so you invest consistently without having to think about it. This strategy is called dollar cost averaging and it works incredibly well over long periods of time.

ALSO READ: What Are the Advantages of Saving Up for Large Purchases?

Final Thoughts: Keep It Simple and Start Now

The mutual fund vs index fund debate does not need to be complicated. For beginners in 2026, the evidence strongly favors index funds. They are cheaper, more tax-efficient, easier to understand, and they outperform the majority of actively managed funds over the long haul.

The best investment you can make right now is the one you actually start. Do not wait until you feel like you know everything. Pick a low-cost index fund, open an account, and put in whatever you can afford. Even $50 a month builds real wealth over time thanks to the power of compounding.

You do not need to be a financial expert to build a strong investment portfolio. You just need to keep it simple, stay consistent, and trust the process. Index funds make all of that a whole lot easier to do.