If you have started investing in dividend paying stocks, you have probably noticed that the numbers on your brokerage statement do not always match what you expected to receive.

Maybe you bought shares partway through the year, or maybe your dividends are getting reinvested automatically and you are not sure how much actual cash landed in your account.

The good news is that calculating cash received from dividends is not complicated once you understand the moving parts.

In this guide, we will walk through exactly how dividends work, how to calculate them step by step, and why this number matters for your taxes and your overall investment strategy.

What Are Dividends and Why Do Companies Pay Them?

Before we get into the math, let us quickly cover the basics. A dividend is a portion of a company’s profits that gets paid out to shareholders. Think of it as a thank you for owning a piece of the business.

Not every company pays dividends. Many growth focused companies, especially in tech, prefer to reinvest profits back into the business instead.

Companies that do pay dividends usually do so on a regular schedule, most commonly quarterly (every three months), though some pay monthly, semi annually, or annually.

The amount paid per share is called the dividend rate, and it is usually expressed as a dollar amount per share, like $0.50 per share.

The Two Main Types of Dividends

There are two types of dividends you will run into as an investor.

Cash dividends are the most common type. The company sends actual money to your brokerage account based on how many shares you own.

Stock dividends, on the other hand, give you additional shares instead of cash. These are less common but do happen, especially with smaller companies trying to preserve cash while still rewarding shareholders.

For this article, we are focusing on cash dividends since that is what most beginner investors deal with.

ALSO READ: 10 Powerful Money Habits of Successful People

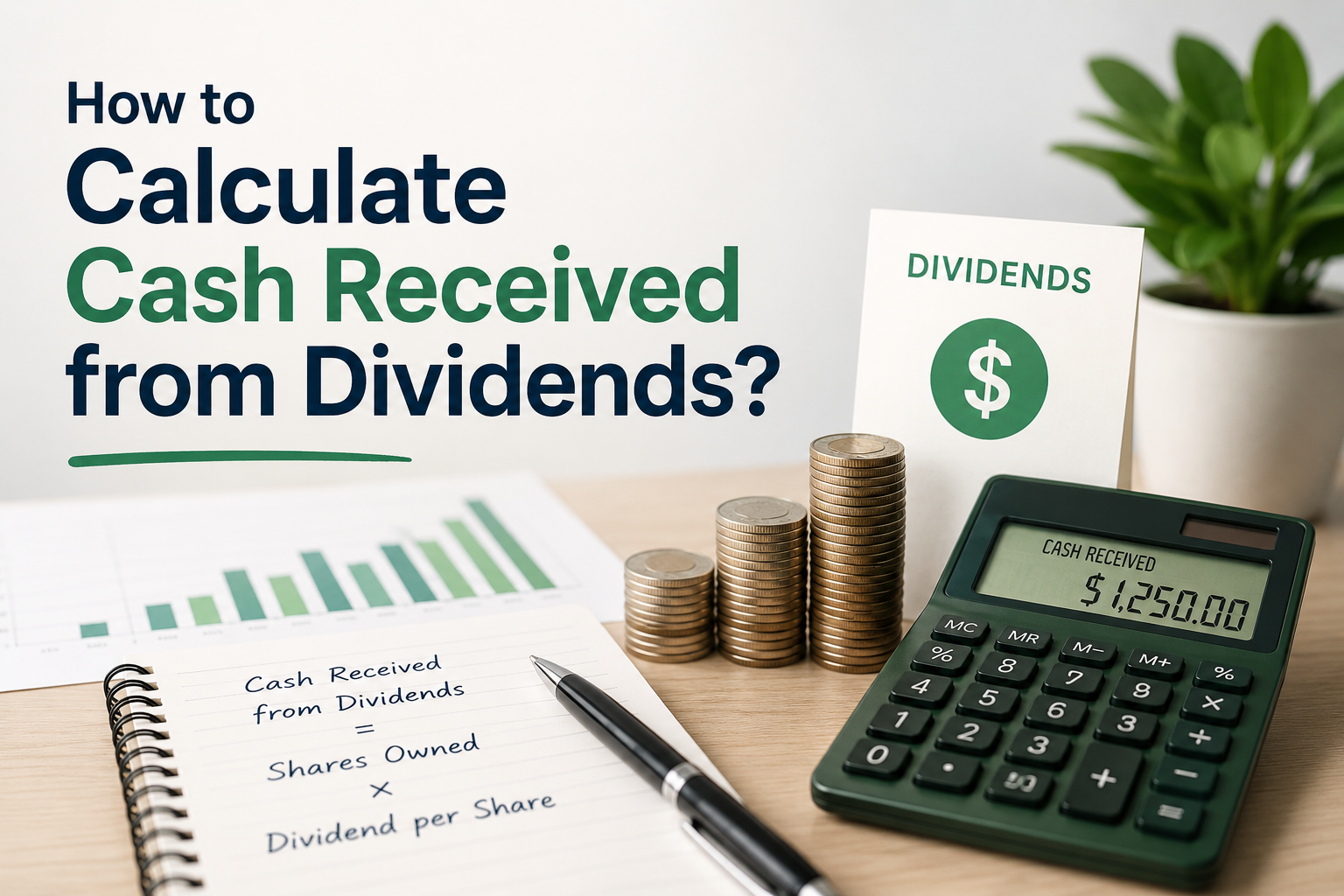

The Basic Formula for Calculating Cash Dividends Received

Here is the simple version of the formula that forms the foundation of everything else in this guide.

Cash received from dividends equals the number of shares you own multiplied by the dividend per share.

So if you own 100 shares of a company, and that company pays a dividend of $0.75 per share, your calculation would look like this.

100 shares multiplied by $0.75 equals $75.

That $75 is the cash that should show up in your brokerage account on the payment date, assuming you have not chosen to reinvest your dividends automatically.

Why the Number of Shares Matters So Much?

This might sound obvious, but it trips up a lot of new investors. The number of shares you own on a specific date, called the record date, determines whether you get the dividend payment at all.

If you buy shares after the ex dividend date (the cutoff date set by the company), you will not receive that particular dividend payment, even if you technically own the stock before the payment date arrives. The previous owner gets that payment instead.

This is important because if you are trying to calculate expected dividend income and you bought shares mid quarter, you need to check whether you owned the shares before or after the ex dividend date for that period.

Step by Step Calculation Process

Let us break this down into a clear process you can follow every time.

Step One: Find the Dividend Per Share Amount

This information is usually announced by the company before the payment date. You can find it on the company’s investor relations page, through your brokerage’s research tools, or on financial websites that track dividend history.

For example, let us say a company announces a quarterly dividend of $0.40 per share.

Step Two: Confirm How Many Shares You Own

Check your brokerage account for your current share count. If you have been adding to your position throughout the quarter, make sure you are using the share count as of the record date, not your current total.

Let us say you own 250 shares as of the record date.

Step Three: Multiply Shares by Dividend Per Share

This is where the actual math happens.

250 shares multiplied by $0.40 per share equals $100.

That $100 represents your gross dividend payment before any taxes are taken out.

Step Four: Account for Taxes if Applicable

In some accounts, particularly taxable brokerage accounts, dividends may be subject to withholding taxes, especially if you are investing in foreign companies. If your broker withholds taxes automatically, your actual cash received will be slightly lower than your gross calculation.

For most US based dividend stocks held in a regular taxable account, taxes are not withheld at the time of payment. Instead, you report the income when you file your taxes.

But if you hold foreign stocks, foreign withholding tax can reduce your actual cash received by 10 to 30 percent depending on the country and any tax treaties in place.

Calculating Dividends Across Multiple Stocks

Most investors do not just hold one dividend paying stock. If you want to figure out your total cash received from dividends across your entire portfolio, you simply repeat the calculation for each holding and add up the results.

Here is a simple example with three stocks.

Stock A pays $0.50 per share, and you own 100 shares. That gives you $50.

Stock B pays $0.30 per share, and you own 200 shares. That gives you $60.

Stock C pays $1.00 per share, and you own 50 shares. That gives you $50.

Add those together and your total dividend income for that payment period is $160.

Using a Spreadsheet to Track Everything

If you own more than a handful of dividend stocks, doing this math by hand every quarter gets tedious fast. A simple spreadsheet can save you a lot of time.

Create columns for the stock name, number of shares owned, dividend per share, payment date, and total cash received. Then add a formula that multiplies your shares by the dividend rate automatically.

As your portfolio grows, you can sort by payment date to see your dividend income laid out month by month, which is incredibly helpful for budgeting purposes if you rely on dividend income.

What If Your Dividends Are Being Reinvested?

Many brokerages offer something called a dividend reinvestment plan, often shortened to DRIP. When this is turned on, instead of cash landing in your account, your dividend payment is automatically used to buy more shares of the same stock.

Here is the important part. Even though you do not see cash hit your account, you still technically received the dividend, and it is still taxable income.

The calculation works exactly the same way. You just need to look at your brokerage statement to see the dollar amount of the dividend before it was used to purchase additional shares.

How to Find This on Your Brokerage Statement?

Most brokerages provide a dividend reinvestment summary that shows the cash value of the dividend, the price per share at which it was reinvested, and the number of new shares you received. This cash value is the number you would use for your calculations, even though the money never sat in your account as cash for more than a moment.

Annual Dividend Income Calculation

If you want to estimate your total dividend income for an entire year, there are two approaches depending on whether the company pays a consistent amount or has a history of increasing dividends.

For companies with a stable dividend, you can simply multiply your quarterly dividend calculation by four, assuming the company pays quarterly. So if you receive $100 per quarter, your estimated annual dividend income would be $400.

For companies that regularly increase their dividend, which many established companies do once a year, your annual total will be slightly higher than simply multiplying the most recent quarterly payment by four.

In these cases, it is more accurate to add up the actual payments you received throughout the year rather than trying to project forward.

Using Dividend Yield to Estimate Future Income

Once you get comfortable with these calculations, you might want to start thinking in terms of dividend yield, which is the annual dividend divided by the current share price, expressed as a percentage.

For example, if a stock pays $2.00 per share annually and trades at $50 per share, the dividend yield is 4 percent.

This is useful because it lets you quickly estimate how much income a certain dollar amount invested might generate. If you invest $10,000 in a stock with a 4 percent yield, you can expect roughly $400 in annual dividend income, assuming the dividend rate stays the same.

Common Mistakes to Avoid

A few mistakes tend to pop up when people first start calculating dividend income.

One common mistake is forgetting to account for shares purchased after the ex dividend date, leading to overestimated income for that period.

Another is confusing the dividend per share with the total dividend payout of the company, which are very different numbers.

The total payout is across all shareholders, while dividend per share is the amount each individual share receives.

Finally, many people forget to factor in taxes when planning their cash flow, especially with foreign dividend stocks where withholding can take a noticeable chunk out of your expected payment.

ALSO READ: What Time Does the Stock Market Open and Close?

Final Thoughts

Calculating cash received from dividends really comes down to one simple multiplication, shares owned multiplied by dividend per share.

The complexity comes in when you start dealing with multiple stocks, reinvestment plans, taxes, and timing around ex dividend dates.

Once you get into the habit of tracking this information, whether through a simple spreadsheet or your brokerage’s built in tools, you will have a much clearer picture of your passive income and how it grows over time.

For anyone building a long term dividend portfolio, understanding these numbers is one of the most satisfying parts of the investing journey, since it gives you a tangible, ongoing reward for the patience you put into your investments.